Analysis of the latest billion-dollar startups points to the emergence of new rules for company valuations

Writing: Paul Hoffman

Once a Silicon Valley invention, the unicorn is now a global creature. The shifting geography and changing industry mix of the world’s most valuable startups tells a bigger story about how innovation in business is now valued.

Unicorns – privately-held startups valued at over US$1 billion – have become a defining currency of modern innovation, and the map of where they emerge is shifting faster than at any time in the past decade. After the exuberance of the late 2010s and the whiplash of the post-pandemic tech boom, today’s unicorn landscape no longer constitutes a California-centric monopoly. Rather, it is a global horse race, shaped by new hubs, new sectors, and a sharp recalibration of investor expectations.

The sector perspective

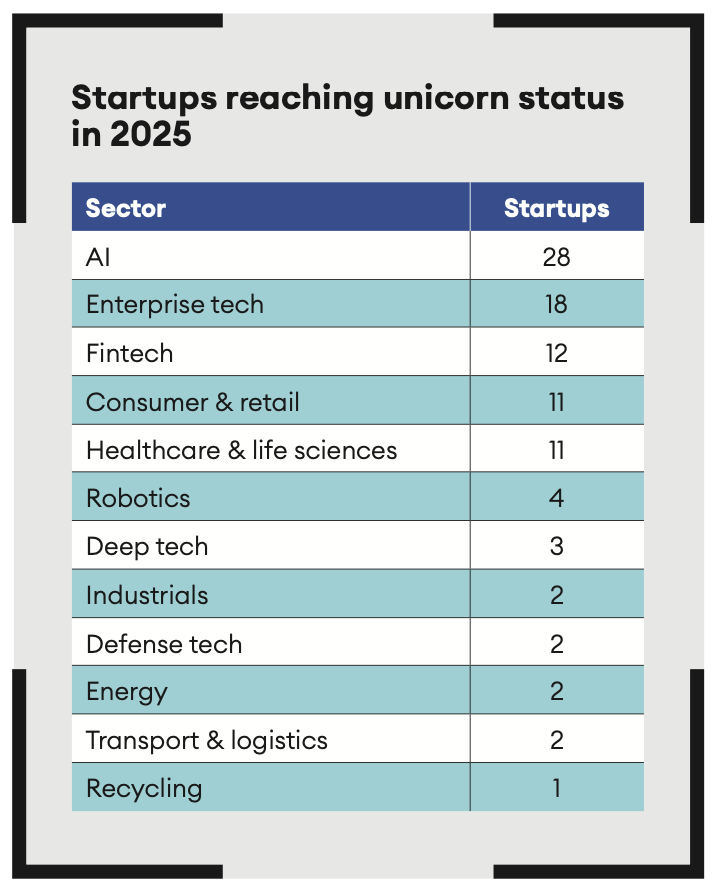

BestBrokers’ analysis, drawing on data from CB Insights, helps to illustrate the shifts now under way. It is no surprise that technology, and AI in particular, are key. In 2025, AI startups accounted for 29.2% of all ‘newly born’ unicorns. Enterprise tech and software accounted for 18.8% and fintech for 12.5%, while consumer and retail, and healthcare and life sciences, each comprised 11.5%.

Fintech led the first major unicorn explosion, and many of its flag-bearers remain among the most valuable private companies worldwide. Stripe,

Klarna, Revolut and Chime turned once-sleepy niches, like digital payments and challenger banking, into billion-dollar juggernauts. Some later successfully went public – yet in general, fintech valuations have cooled. Klarna’s value plunged from $45.6 billion in 2021 to about $6.7 billion in 2022, before rebounding to $18 billion when it went public in 2025. Despite this, 12 fintech startups reached a valuation of $1 billion or more during 2025 – 12.5% of all 96 unicorns that were ‘born’ and remained private throughout the year. This makes fintech the third-most common industry for modern-day unicorns, and the sector continues to mint new stars, especially in emerging markets. Mexico’s Plata and Kapital reached unicorn status during 2025 with valuations of US$3.1 billion and $1.3 billion, respectively.

Yet the torch has unmistakably been passed to AI. The release of ChatGPT in late 2022 sparked a global boom, making AI the fastest-growing engine of unicorn creation in history. OpenAI’s half-trillion-dollar valuation, Anthropic’s rapid fundraising, and the rise of enabling infrastructure firms like Hugging Face and CoreWeave pushed AI to the center of private markets. Venture investment was quick to follow: nearly one in two new unicorns worldwide in 2024 had an AI angle, spanning generative tools, chip design, automation, or sector-specific models for finance and healthcare. The latest figures suggest the shift is only accelerating – but the peak is still yet to come.

Even biotech startups, long considered a separate universe, now regularly integrate AI platforms to speed up drug discovery or assist in medical tech, creating hybrid AI-biotech unicorns such as the American Insitro, Sweden’s Neko Health, and Singapore’s UltraGreen.ai.

There’s been a decline in another once-promising field, however: green tech. Climate- and renewable-focused startups used to sprout across Europe and the US, thanks to government incentives, corporate net zero mandates and rising energy insecurity. Now, with the Trump administration rolling back or threatening key green incentives from the Biden-era Inflation Reduction Act, the momentum has slowed. Clean-energy projects worth more than US$14 billion were canceled or delayed during 2025, and the Financial Times has noted a trend for “greenhushing,” where companies scale back green bonds – or avoid labeling them green – to minimize political risk.

The ramifications are evident across the market. Earlier this year, Swedish battery maker Northvolt filed for bankruptcy and, although rescued by an acquisition, the incident dealt a major blow to Europe’s battery ambitions. It also rattled confidence among startups more broadly. Funding is no longer so easily secured, no matter how promising a project may sound. According to Crunchbase, cleantech startups have seen a 46% drop in investment in 2025 versus the same period in 2024. Capital is getting more selective: investors want not just ideas but demonstrable paths to revenue.

The new geography

Just as the sectors driving the growth of unicorns have diversified, so the geography of unicorn creation has undergone its own disruption. California’s Silicon Valley – and the US as a whole – still dominates: nearly a quarter of the current 1,321 unicorn startups worldwide are based in the Golden State.

This dominance no longer resembles the 2010s, however. Several European cities, including London, Paris and Berlin, have positioned themselves as major entrepreneurship hubs. One of the most intriguing unicorns to emerge from the UK recently is the AI-infrastructure company Nscale, which raised $1.1 billion in a Series B round in September 2025.

And if AI isn’t appealing enough, Nscale also runs its data centers on 100% renewable energy. That makes for an irresistible cocktail of buzzwords, which has led investors such as Blue Owl Managed Funds, Dell, Nvidia and Nokia to put actual capital into the startup. The list is hardly surprising, considering Nscale’s work on OpenAI’s Stargate data centers, including a major AI campus in Norway.

Asia’s story is even more dramatic. Chinese and Indian cities now regularly mint unicorns with regional and increasingly global ambitions. Despite the lack of Western investor capital flowing into China, cities like Beijing, Shanghai, Hangzhou and Shenzhen host more valuable startups than most of Europe.

The new value equation

Behind these sectoral and geographic shifts is a change in how investors define value. The AI boom inflated valuations at a pace that startled even seasoned venture capitalists, and many now expect a correction – not only in private funding, but potentially across global markets.

Signs of this are already visible: 2025 produced fewer unicorns than 2021 and 2022, though more than 2023 and 2024. Enthusiasm for AI remains intense, but these numbers show a maturing market where sector dominance is concentrating rather than dispersing.

If the past decade was defined by the race to create as many startups as possible, the next few years will be defined by competition that determines which ones endure. We may need to look past hype cycles toward businesses with global relevance; past hot markets and toward genuine problem solvers. That shift may prove to be the healthiest development the startup world has seen in a long time.

Paul Hoffman is data analyst and author at the finance research and analysis platform BestBrokers.com