Financing projects via crowdfunding involves choosing the right model, researching competitors, planning your campaign and keeping your crowd enthused and updated, writes Chris Buckingham

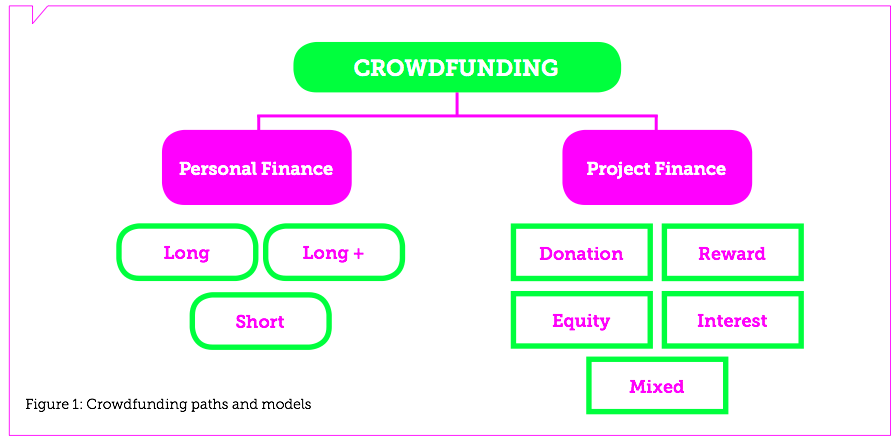

Crowdfunding is a very generic term but there are two distinct “paths” to the concept; consumer lending (where consumers raise debt for things like a car) and project finance (where people raise funds for all sorts of projects).

It becomes confusing as each path also has its own set of “models” that hang like fruit beneath it (see figure 1 overleaf):

I am going to concentrate on the project finance path on the right-hand side of the diagram, but before I do, it’s important to explain the personal finance path and models first. There are three models in this path:

Long – which is debt taken and lent for longer periods of time (typically three-to-five years), where the capital is paid back with high street bank equivalent rates of interest.

Long+ – a hybrid model where lenders can lend for longer periods of time but they are lending to very high risk individuals and so the rates reflect this and are very high. Really this is a fusion of long and short models.

Short – is payday or vulture lending, typically for very short terms at very high rates of interest.

Without getting into the ethics of the short model it should be noted that the two main platforms (the Lending Well and Piggy Bank) are not presently accepting further funds from the public.

Let’s now leave the personal finance path and turn to the project finance path. I use the term “project” rather than “entrepreneurial” or “business” path as there is an issue of sustainability in these projects. Some (about 20% of my clients) are creating a short-term project that is ephemeral in nature. In other words, it is a short- lived artistic or community-based project that exists to achieve some localised goal and then ends.

The intention for the management behind these projects is not to be the next Dyson or Facebook but rather to create some form of value for their (often local) network. The term project then becomes all encapsulating in that it also includes bigger projects looking to raise serious amounts of cash as well as these local causes with a much smaller scale.

For ease of use I also use the acronym DREIM to help remember the models in the project finance path, this stands for:

Donation – straightforward philanthropy

Reward – where funders receive a gift for their financial input

Equity – shares are now offered for the crowd’s financial input

Interest – the raising of debt by established firms (often with security)

Mixed – which is often a blend of reward with equity or interest. Motivations change in each of the DREIM models and this is important if you are considering crowdfunding your project.

Choosing the model that is right for your project is not that easy – and there are many factors to consider before a decision is made. These relate to the business model, the value that management can offer the crowd through their crowdfunding activities, and the perceptions that the crowd is likely to have of the project.

To give a clear example, I recently helped an engineer successfully raise funds to enable the tooling and build of a unique outdoor product. The initial consultation was to see if the management behind the product could use the reward model and thus avoid having to lose a degree of control through giving away equity.

The interest model was not an option as they had been trading less than two years (a standard requirement) and they were also reluctant to offer personal guarantees. The donation model was not an option either as they were a limited partnership and not a charity or community interest company (some platforms also accept co- operatives). So the reward model was the most attractive model to the management team.

Having eliminated the other models, the next step was to audit the reward platforms (the websites offering this service) and look at the other crowdfunding campaigns that were active on these platforms. The questions I needed to address were:

- Was there a similar product on the platform?

- Was it succeeding?

- For how long had it been campaigning?

- When did it launch (seasonality)?

- How much was it trying to raise?

- What gifts was it offering?

- How was the campaign structured (for example, video, updates, use of social media)?

- Which platform had it used?

By recording as much of this information as possible we were able, pretty quickly, to eliminate some of the smaller platforms and start to focus our research on the most likely platforms that would lead to the project reaching it’s funding target. These targets, of course, vary from campaign to campaign. Some crowdfunding campaigns are only seeking a very small amount (my lowest campaign has been for £300) while others are seeking a great deal more (my highest so far has been £1.6 million).

Note too, that I use the term “campaign” to talk about crowd- funding activities. This is because what management is really doing, when it attempts to crowdfund a project, is asking the crowd for permission to create the vision it is proposing. I call this ‘crowdconsent’, because the crowd is being asked to give its consent to the creation of the vision.

The activities that are involved in any campaign are pretty much standard across the different models. These involve:

- Video – a presentation of the product and the team

- Main page pitch – the text that will present the product and the team

- The promise – this could be the gift in the reward model, the share class in equity or the level of interest tolerance in the interest model

- Updates – these are in the form of responses to questions from the crowd or progress reports or appreciation to the crowd for its financial input

These four areas need careful planning long before you launch. Standard practice is to start the planning at least eight weeks prior to launch. Failure is still common in crowdfunding (nearly 60% in some estimates) so putting as much as possible of the planning and strategy in place before you launch is vital.

This should also include attracting high net worth investors. The more money the management can attract early in the campaign, the better. Levels of pre-crowdfunding investment range from 15% to 40% – but the reality is the more money that has been promised to the campaign by members of your personal and professional network before launching, the better.

The reason for this is that it acts as a motivator for the crowd. Members of the crowd have their own subjective perceptions and make their own judgments about the campaign. Each member of the crowd will possess separate bits of information they have managed to glean from the wording in the video, of the accounts or the business plan or from any other piece of the puzzle they have scrutinized.

So by getting investors involved nice and early, the management team is sending a signal to the crowd that says: “Hey, look at us, we must have something good here as we already have £X invested.” This is echoed in the need for updates and keeping the crowd informed about what’s going on with the project. While the campaign is running, it is essential that management keep the crowd informed through regular contact (at least three times a week).

This contact can be via the platform itself (in the case of the reward model, these are called updates and are often comments made by the crowd; in the equity and interest models they are more likely to be questions posed directly to the management team) or through other external social media channels such as Facebook, Twitter and LinkedIn. These points of contact are important as they enable issues and concerns the crowd may have to be addressed.

For example, a very early campaign on which I was working, was raising debt, using the interest model. The company launched the campaign and all was progressing as expected when, on day three, a question from the crowd was addressed directly to one of the directors of the company. The question was: “How strong is your relationship with your spouse?”

At first glance, this question may seem a really odd thing for someone considering an investment in the company to ask. But what this member of the crowd had spotted was the £50,000 that had been leant to the company within the past 12 months. Suddenly, the relevance of the question becomes very clear.

But this also raises another important point regarding addressing questions or providing updates about the project. It must be remembered that although the question has been asked by a specific person and the response is addressed to this one specific person – the response is open for scrutiny by the crowd. Care must be taken to craft a response or make an update that is relevant and balanced, so as not to offend or make claims that are false.

Chris Buckingham is a crowdfunding researcher, who has worked on wide-ranging campaigns related to everything from the arts to zoos. He has contributed to more than £2 million worth of crowdfunding activity and is in the process of publishing the first book to cover all five models in the ecosystem. With a background in the management of the creative and cultural industries, he was one of the early users of crowdfunding and still finds the sector fascinating as more applications and models emerge. He lectures at Winchester School of Art and University of Winchester on this, and related topics.